Russia’s termination of natural gas transit via Ukraine on January 1, 2025, marks a major shift in Europe’s energy landscape, with serious economic and geopolitical consequences. Gazprom cites the expiration of the transit deal and Ukraine’s refusal to renew it, cutting off nearly half of Russia’s gas supply to Europe.

With Ukrainian transit accounting for 4.5% of EU gas consumption, the disruption threatens market stability. The January 1, 2025, closure of the Ukrainian transit route has intensified the crisis. While once a secondary supply channel, its importance has grown following the shutdown of Nord Stream and the Belarus-Poland pipelines. Eastern European nations—Hungary, Slovakia, and Austria—are particularly exposed.

Negotiations for alternative gas routes have largely failed. Ukraine’s refusal to renew the transit deal or accept rerouted Russian gas has left Europe scrambling. Proposals to channel gas through Azerbaijan or resell Russian supply at the border face logistical and political roadblocks, fueling market instability.

While U.S. LNG exports have increased, replacing Russian pipeline gas remains uncertain. LNG is costlier, less reliable, and logistically complex, potentially exacerbating Europe’s energy vulnerability. Greater reliance on LNG may lead to supply bottlenecks and sustained high prices.

Europe faces a deepening energy crisis as an unexpectedly harsh winter, weak renewable output, and the shutdown of Russian gas transit via Ukraine collide. December 2024 saw a sharp drop in wind power generation, with Germany’s wind output plunging 85% from the previous year. This shortfall has forced greater reliance on fossil fuels, particularly natural gas, to sustain heating and electricity needs.

Electricity prices have soared—UK rates hit £485/MWh in last mid-December, far above the 2023 average of £70, while German prices doubled year-over-year. Gas reserves are depleting rapidly, falling below the five-year average by late December. Maxar Technologies warns of further cold spells in January, exacerbating supply pressures.

The 3.35% rise in European TTF gas futures on December 31, 2024, to 50.53 euros signals immediate market anxiety. The memory of the 2022 crisis, when prices surged 100–200%, heightens concerns over another energy shock. Europe’s economic recovery remains fragile, and soaring energy costs could reignite inflation and industrial slowdowns.

With demand set to rise in January, Europe’s dependence on natural gas, weak renewable output, and geopolitical deadlock underscore its energy vulnerability. High costs and strained supply chains could define the continent’s toughest winter in years.

EU-US tensions have escalated after Trump’s ultimatum, demanding greater European reliance on American oil and gas under threat of tariffs. European Commission President von der Leyen signaled openness to increasing US LNG imports after Trump’s election, reflecting the EU’s evolving energy strategy. The shift is evident: Russia’s 41% share of EU gas imports in 2021 fell sharply, while the US rose to 16% by mid-2024, second only to Norway.

The launch of the Plaquemines LNG export facility in Louisiana—the largest in the US—marks a major step in expanding American gas exports. Its first shipment left in late December 2024 and is expected in Germany by early January. With Russia’s Ukrainian pipeline shut, the US is poised to fill the gap, but challenges remain. Delays in US export facilities and Europe’s rapid gas inventory depletion amid a harsh winter have tightened the market, limiting short-term relief.

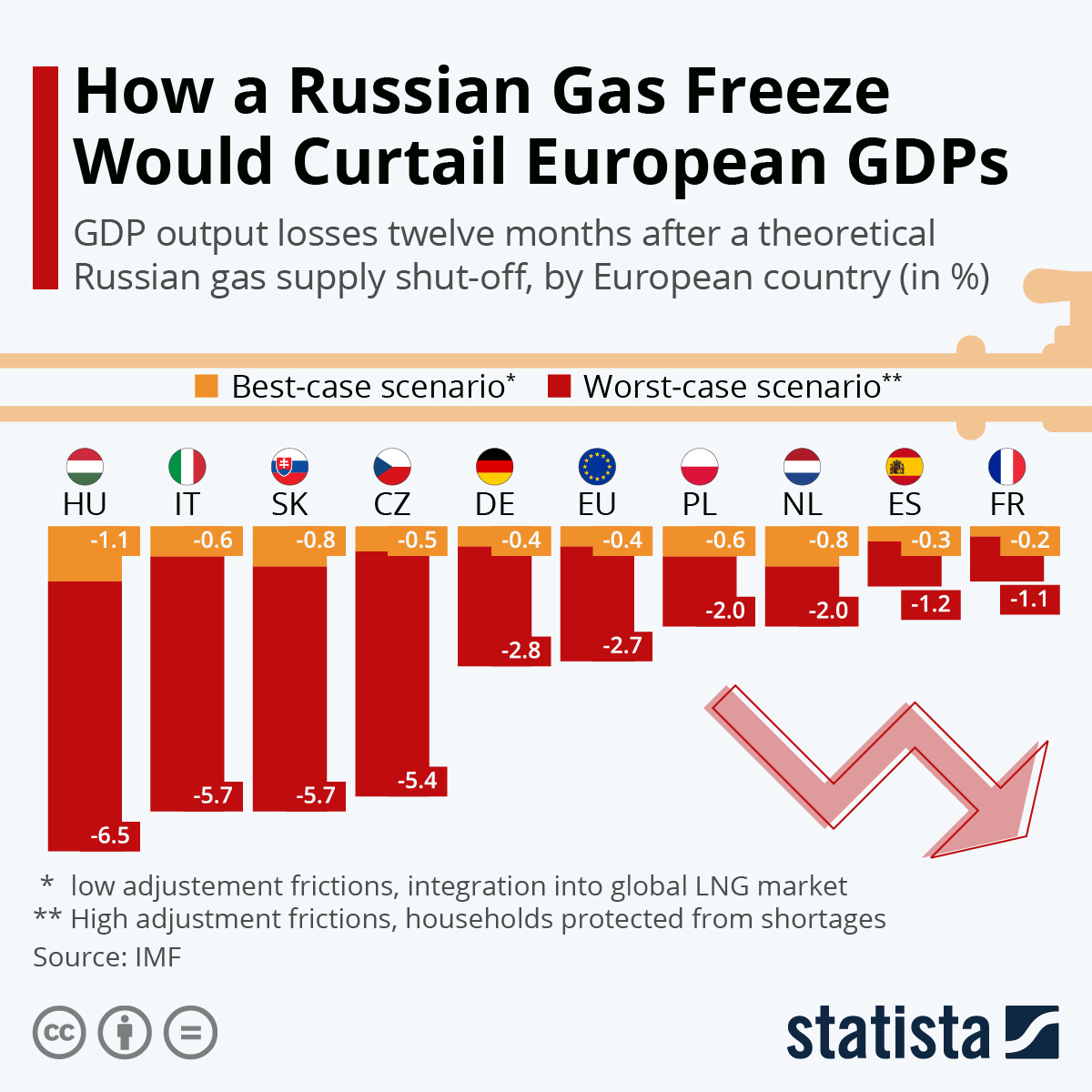

Europe has steadily reduced Russian energy dependence since the Ukraine conflict, strengthening its ability to withstand disruptions. This strategic decoupling has emboldened the EU to consider further sanctions on Russia. However, the sudden pipeline closure will strain member states like Hungary, which remain heavily dependent. Rising LNG transport costs and infrastructure constraints add to concerns over price volatility and economic strain.

In the long term, the EU’s pivot toward US LNG and diversified energy sources signals a broader geopolitical realignment. Yet, short-term supply risks and rising costs expose Europe’s continued energy vulnerability in an increasingly unstable global landscape.

The global natural gas market is shifting, with 2025 expected to bring both increased supply and continued volatility. Following the shortages of 2022 and price spikes during Asia’s 2024 heatwaves, the key question remains: will shortages return in 2025?

Market projections indicate ample supply. The World Bank forecasts 2.3% global natural gas growth, while S&P Global expects an additional 27 million tons of LNG, driven largely by North American projects.

However, risks remain. Trump’s energy deregulation and infrastructure expansion could exacerbate oversupply. If Russia-Ukraine tensions ease and sanctions lift, downward price pressure may intensify. Potential disruptions—strikes, natural disasters, or bottlenecks at LNG terminals— could destabilize markets, as seen in the 2023 Australian LNG strike that spiked European prices by 10%.

The concentration of new capacity among the US, Qatar, and Australia—set to supply over 60% of global LNG—adds another layer of risk. Any disruption in these hubs could trigger supply chain shocks, amplifying volatility.

Climate extremes further complicate forecasts, temperature swings could drive sudden demand spikes, while global market interconnectivity means local shocks ripple worldwide.

While 2025 promises increased supply, the market’s structural fragility—geopolitical risks, supply chain vulnerabilities, and climate-driven demand surges—suggests that price swings and instability will persist.

Source: BBC, Statista, ISPI