In the past two years, China’s photovoltaic industry capacity has tripled, but the profit margin has fallen by 70%.

Due to super large-scale manufacturing and fierce market competition, China’s photovoltaic manufacturing costs are far lower than those in Europe, America, India, and other major countries. There are continuous technological advancements, including N-type TOPCon, BC batteries, Calcium Titanium Ore, and hundreds of other technologies. The conversion efficiency and effectiveness of China’s photovoltaic equipment, adhesive films, and auxiliary materials are world-leading, and the industry chain is complete.

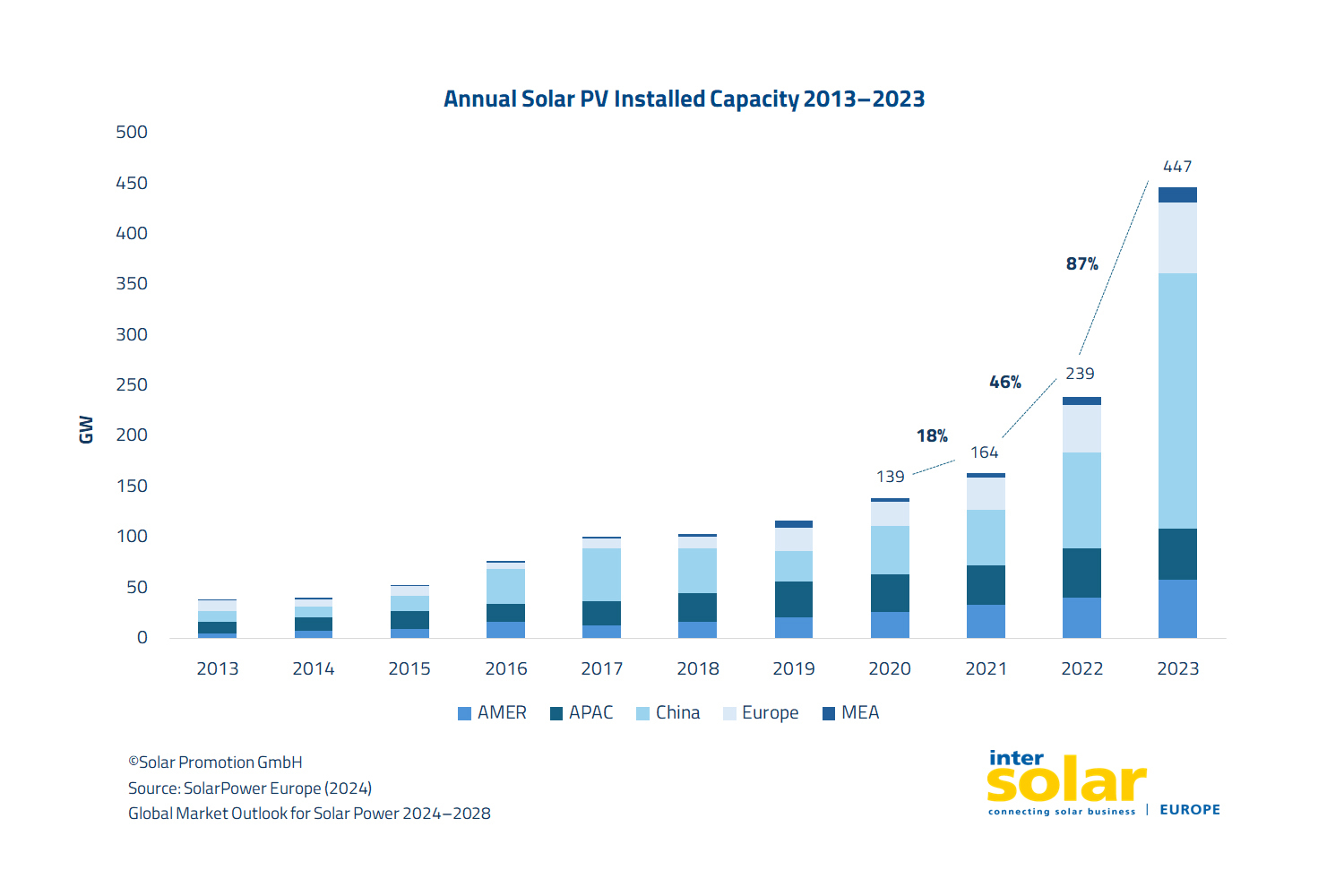

As of 2023, China’s annual production includes 1.43 million tons of silicon, 622 GW of silicon wafers, 545 GW of batteries, and 499 GW of components, all of which rank first globally. Component production capacity exceeds 80% of the world’s total. The enormous production capacity can only be absorbed by exporting to the global market.

Production capacity at home and the market overseas has been a significant challenge for China’s photovoltaic industry. Before 2011, 57% of China’s photovoltaic products were sold to Europe, 15% to the United States, and only 6% to the domestic market, with even the whole of Asia being relatively inactive.

Source: SoloarPower Europe

However, in 2011, the European and American anti-dumping and anti-subsidy investigations brought a catastrophic blow to Chinese photovoltaic enterprises, causing major companies like Suntech Power to go bankrupt.

Policy changes in Europe and the United States have been a nightmare for the Chinese PV industry. To avoid these reviews, since 2014, leading enterprises have built factories in Southeast Asia to sell to Europe and the United States, marking the first stage of photovoltaic expansion overseas.

The United States, in an effort to limit the development of China’s photovoltaic industry, has raised tariffs and restricted imports while heavily subsidizing local enterprises. On May 14, the White House announced that, on top of the original Section 301 Tariff Action on China, tariffs on Chinese imports worth $18 billion would increase from 25% to 50% for solar cells. Furthermore, to prevent China from exporting photovoltaics through Southeast Asia, the United States initiated anti-circumvention investigations in four Southeast Asian countries, and tariff exemptions for these countries expired on June 6 this year.

At present, Jinko Solar, LONGi Green Energy, Trina Solar, and other giants have deployed at least 26 GW of silicon wafer production capacity, 60 GW of battery production capacity, and nearly 50 GW of component production capacity in Southeast Asia, accounting for more than half of the total local production capacity. These are mainly exported to the United States. However, with the United States imposing tariffs on Southeast Asian imports, the local photovoltaic industry is facing significant challenges.

Source: Caixin Global

On the other hand, the United States, through the enactment of the Inflation Reduction Act, allocated $7 billion to the Solar for All program for tax credits, subsidies, and other economic incentives. However, to qualify for the 17 cents/W subsidy, products must be manufactured in the U.S., clearly aiming to limit the competitiveness of Chinese PV enterprises in the American market. The most iconic event in this context is that U.S. company First Solar, despite having outdated technology and ranking only tenth in global module shipments, has become the world’s largest PV stock by market capitalization.

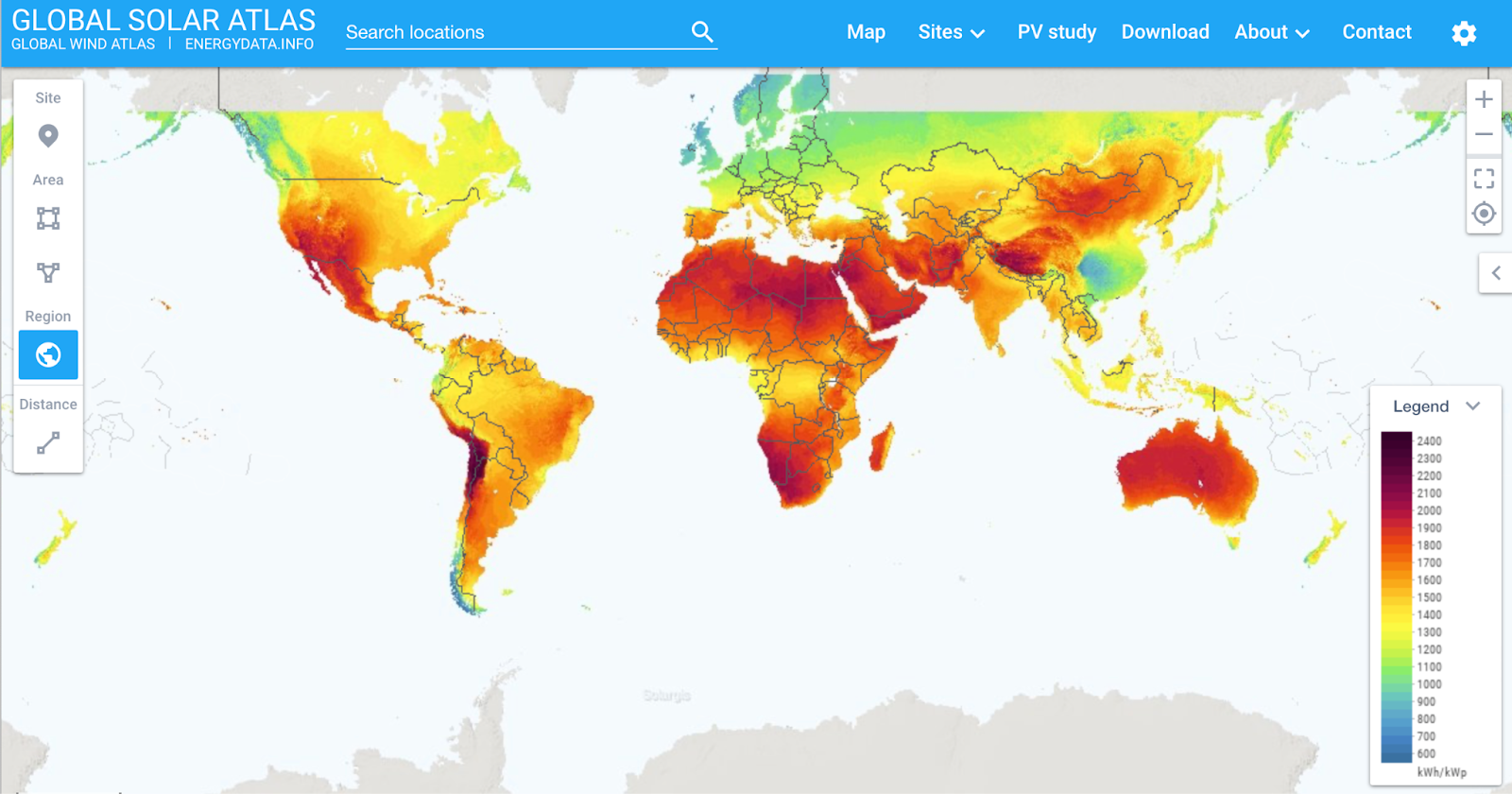

Since 2023, waves of Chinese delegations have visited the Middle East seeking investment opportunities. The Middle East’s climate is dominated by tropical deserts, with almost all areas receiving very high levels of solar radiation energy. The region is a natural fertile ground for the development of solar energy.

Source: Global Solar Atlas

From 2012 to 2021, the growth rate of total installed renewable energy capacity in the Middle East was only 76%, much lower than the world average of 112%. By the end of 2021, the global installed renewable energy capacity was 3,587 GW, while the Middle East’s capacity was only 24 GW, less than 1% of the global total.

With the advancement of dual-carbon goals, the global transition to clean energy has accelerated. The UAE has released Energy Strategy 2050, which aims to increase the share of clean energy to 50% by 2050 and achieve net zero greenhouse gas emissions by the same year.

The Saudi Vision 2030 states that by 2030, exports of non-oil energy will increase from 16% to 50% of GDP, aiming to increase non-oil revenues sixfold. Additionally, by 2030, Jordan plans to increase the proportion of renewable energy generation to 31%, and Oman plans to reach 20% renewable energy consumption, increasing to 35%-39% by 2040.

Among these efforts, photovoltaic energy is the most important new energy direction. Saudi Arabia plans to increase its installed PV capacity to 40 GW by 2030. If this target is realized, Saudi Arabia will be among the top 5 PV markets in the world. The country’s installed capacity in 2023 is only 7 GW, meaning it needs to increase nearly fivefold in the next seven years.

With huge production capacity, leading technology, and efficiency, China’s PV industry is well-positioned to thrive in the Middle East. This represents a mutually beneficial collaboration between large-scale supply and large-scale demand.

In the past two years, China’s photovoltaic products have accelerated their entry into the Middle East. From 2022 to 2023, China’s exports of photovoltaic modules to the Middle East and North Africa consecutively exceeded 10 GW, with Saudi Arabia and the United Arab Emirates showing rapid growth. TCL Central and Trina Solar decided to build factories in Saudi Arabia last year. In May 2023, TCL Central and Saudi Vision Industries reached a strategic cooperation to establish a joint venture for PV manufacturing.

Additionally, China Energy Engineering Group has secured the contract to build a 2.6 GW PV power plant in Al Shuaibah, Saudi Arabia, the largest single PV power plant project under construction worldwide. Covering an area of 53 square kilometers, the project will feature over 810,000 piles and more than 5 million PV panels, visible even from satellite imagery.

In 2024, China’s momentum in the Middle East remains strong. In April this year, China exported 2.3 GW of modules to the Middle East, a 142% year-on-year increase. From January to April, cumulative exports totaled about 10.3 GW, a year-on-year surge of 188%, with Saudi Arabia purchasing 1.4 GW in April, accounting for 59% of the Asia-Pacific market.

Source: powerengineeringint, Xinhua