Over the past four decades, the Federal Reserve’s monetary policy has been shaped by a succession of chairpersons, each responding uniquely to the economic challenges of their respective eras.

From Paul Adolph Volcker’s aggressive rate hikes to combat inflation, to Alan Greenspan steering the U.S. through periods of economic expansion, to Ben Shalom Bernanke’s use of quantitative easing in response to the global financial crisis, and Janet Louise Yellen’s initiation of the interest rate hike cycle, each leader has left a distinct imprint on the Federal Reserve’s history. Today, the Fed faces one of the most complex global economic landscapes in modern times.

On 18 September, Chair Jerome Hayden Powell made a historic move by announcing a 50 basis point rate cut, signaling the start of a new easing cycle.

The critical question now is whether Powell can replicate the success of his predecessors and guide the U.S. economy to a soft landing. What legacy will he ultimately leave in the annals of economic history?

The Volcker Moment: Taming Inflation at the Cost of Recession

In the late 1970s, the U.S. was entrenched in stagflation, characterized by stagnant economic growth and persistently high inflation. Confronted with this severe economic dilemma, then-Federal Reserve Chairman Paul Volcker implemented an unprecedented policy of aggressive interest rate hikes.

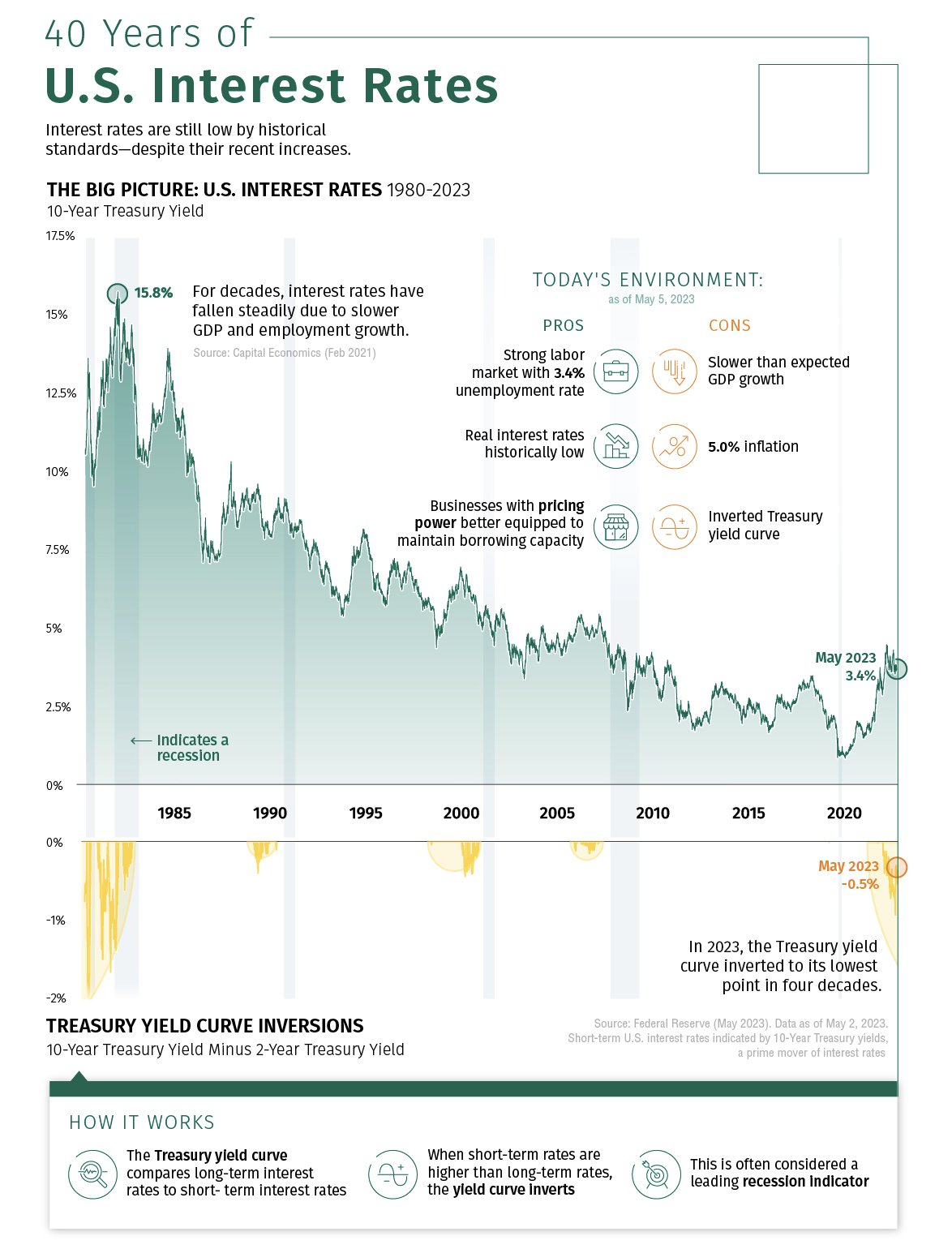

Between 1981 and 1990, the federal funds rate soared to an all-time high of 19-20%. While this drastic move successfully curbed inflation, it also triggered a recession, with unemployment peaking at nearly 11%—the highest level since the Great Depression.

During this period, the Fed’s interest rate adjustments were highly volatile. On November 2, 1981, the target rate dropped sharply to 13-14%, only to rise again to 15% in early 1982, before falling back to 11.5-12% by July of the same year. Despite these fluctuations, the “effective” federal funds rate averaged 9.97% over the decade. After November 1984, the rate did not surpass 10%.

Unlike today’s approach to inflation control through direct interest rate adjustments, Volcker’s strategy focused on limiting the growth of the money supply. Though heavily criticized at the time, his policy eventually reduced inflation to below 2% by 1986, solidifying his legacy as a key figure in taming inflation.

Alan Greenspan: Mastermind Behind the U.S. Economy’s Soft Landing

Alan Greenspan, who served as Chairman of the Federal Reserve from 1987 to 2006, played a pivotal role in shaping U.S. monetary policy, managing the domestic economy, and influencing global economic affairs.

In August 1990, the U.S. entered an eight-month recession, during which Greenspan led the Federal Reserve through a successful response, culminating in a federal funds rate increase to a then-record high of 6.5% by May 2000. By contrast, interest rates had dropped to a decade-low of 3% by September 1992, reflecting the Fed’s adaptability in response to changing economic conditions.

In 1995, Greenspan skillfully navigated the U.S. economy to a soft landing, laying the groundwork for the economic expansion that followed. Notably, in 1994, the Fed raised interest rates sharply to counter inflationary pressures, which contributed to a significant cooling of the labor market. By May 1995, employment growth had turned negative, prompting the Fed to cut interest rates by 25 basis points on three separate occasions between 1995 and early 1996. This strategy proved effective, with average monthly job creation rebounding to approximately 250,000 by mid-1996, and inflation remaining under control for an extended period thereafter.

Greenspan’s 18-year tenure is the longest in the Federal Reserve’s history, during which he successfully guided the U.S. economy through its longest period of expansion at the time. Under his leadership, the Fed also informally introduced a 2% inflation target, a move that has since had a lasting influence on modern monetary policy.

Ben Bernanke: The Architect of Open-Ended QE

At the onset of the 2008 financial crisis, Federal Reserve Chairman Ben Bernanke spearheaded a historic intervention by implementing quantitative easing (QE) and slashing interest rates to near zero in an effort to rescue the U.S. economy from collapse.

Prior to the crisis, interest rates had peaked at 5.25%. However, in response to the subprime mortgage meltdown, the Federal Reserve swiftly reduced rates by 100 basis points, bringing them close to zero.

During this period, the Federal Reserve introduced a policy of quantitative easing, formally referred to as Large-Scale Asset Purchases (LSAP). This strategy aimed to lower long-term interest rates and stimulate economic recovery by purchasing large amounts of government and mortgage-backed securities. As a result, the Fed’s balance sheet expanded dramatically, growing from $870 billion to an unprecedented $4.5 trillion.

It wasn’t until 2015 that the Fed began cautiously raising rates by 25 basis points at a time, with the target rate gradually reaching 2.25-2.5% by 2018.

Yellen: Navigating from QE Exit to Rate Hike Cycle

In February 2014, Janet Yellen succeeded Ben Bernanke as Chair of the Federal Reserve, guiding the U.S. economy through the later stages of recovery from the Great Recession.

Beginning in December 2015, Yellen initiated the first interest rate hike in nearly a decade, raising the federal funds rate by 25 basis points annually until 2017. In 2017, the pace accelerated, with the Fed raising rates three times, followed by four rate hikes in 2018. By the end of Yellen’s tenure, the federal funds rate had peaked at 2.25-2.5%.

Powell Takes the Stage: Where is the U.S. Economy Headed?

In February 2018, Jerome Powell assumed the role of Chairman of the Federal Reserve. Confronted with lukewarm inflation and slowing economic growth, the Fed opted to cut interest rates three times in 2019 to rejuvenate the economy, mirroring Alan Greenspan’s rate cuts from the 1990s.

This approach continued until the onset of the COVID-19 pandemic, which marked the beginning of a new economic era. In response to the crisis, the Fed swiftly reduced interest rates to near zero during two emergency meetings held within 13 days.

In the aftermath of the pandemic, inflation reemerged as the primary economic threat facing the United States. In March 2022, the Fed raised interest rates for the first time in over three years, implementing a 25 basis point increase. Over the following year, the Fed adopted an aggressive stance, raising the benchmark interest rate to a peak of 5.25-5.5%.

Recently, the Fed made its first rate cut since April 2022, setting the benchmark rate at 4.74%-5%. Scott Sumner, the Ralph G. Hawtrey Chair Emeritus of Monetary Policy at the Mercatus Center at George Mason University and Professor Emeritus at Bentley University, pointed out that central banks tend to focus on winning the last war. If inflation is high, a tougher stance is taken. If inflation is below target, the Fed will be more expansionary. Powell came into office determined that if there were another recession, the Fed would adopt a more aggressive policy. Personally, he believes that strategy was relatively successful at first, but it ultimately went too far.

Source: mercatu, CNBC, the New York Times, visualcapitalist, Bank Rate