The agreement between Gazprom and Ukrainian oil and gas companies on the import of Russian gas into Europe via Ukraine will expire on 31 December this year. The agreement allows Russian gas to continue to be transported through Ukrainian territory even after the full escalation of the Ukrainian crisis in February 2022, and it is the only surviving trade agreement between Russia and Ukraine at present. However, the deal is facing an end.

On 27 August, Ukrainian President Zelensky said at a briefing that Ukraine does not intend to extend the gas transit agreement with Russia, and that it is ready to discuss obtaining gas from other suppliers through its gas transport system at the request of Europe. What does it mean that the Ukrainian government has strongly stated at a high level that it will not renew the agreement?

Historical Russian-Ukrainian gas relations

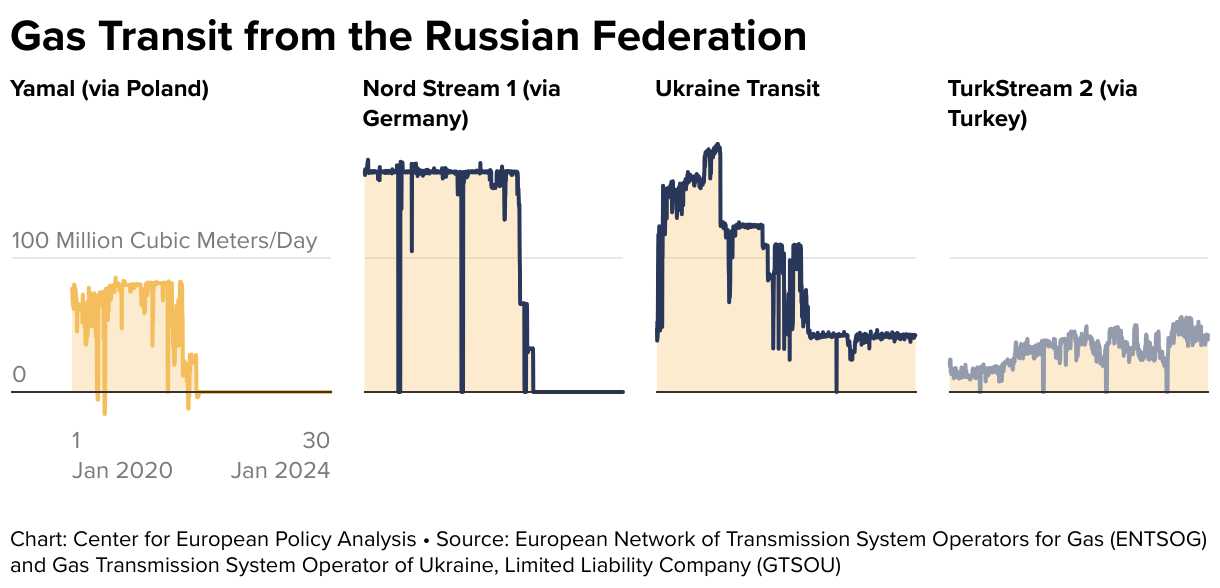

Before the full escalation of the Ukrainian crisis, Russia was the EU’s largest natural gas supplier, accounting for 43% of its imports. Several gas pipelines transport Russian gas to Europe, including the Nord Stream pipeline, which runs through the Gulf of Finland and the Baltic Sea to Greifswald in Germany. Other pipelines transit through third countries, with two passing through Belarus and Poland, and two through Ukraine. Additionally, two pipelines run through Turkey.

After the Soviet Union’s collapse, the energy relationship between Russia, the EU, and Ukraine became a crucial element of European geopolitics. Ukraine, as a key transit country, received high transit fees and favorable gas prices from the Russian-European gas trade. Under a barter agreement, Russia provided Ukraine with 17 billion cubic meters of gas annually in exchange for transit fees, while selling an additional 8 billion cubic meters at a preferential price.

However, the Orange Revolution in Ukraine in 2004 drastically altered the traditional Russian-Ukrainian gas relationship. Ukraine increasingly aligned with the EU in the geopolitical rivalry with Russia, leading to multiple disputes over gas prices and transit fees between 2006 and 2009. Russia sold gas to Ukraine at a market price of $230 per 1,000 cubic meters, compared to the previous subscription price of $50 per cubic meter. These conflicts occasionally disrupted Russian gas supplies to Central and Eastern Europe, causing severe shortages in several Western European countries.

In November 2013, Ukraine’s intent to sign an association agreement with the EU triggered a further escalation in the Russian-Ukrainian gas dispute, culminating in the Ukrainian crisis. Following the Crimean crisis in 2014, Russian gas deliveries to Ukraine reverted to a “political price” of $485 per 1,000 cubic meters, with a mandatory prepayment mechanism introduced.

Ukraine accused Russia of “economic aggression” due to the sharp price increase. In June 2014, Gazprom cut off gas supplies to Ukraine after it failed to meet the advance payment deadline. After nearly six months of interruptions, Ukraine repaid its $3.1 billion gas debt in two installments by the end of 2014, leading to the resumption of gas supplies.

In 2019, Russia and Ukraine signed a gas transit agreement, allowing Gazprom to export gas to the EU through Ukrainian pipelines. However, following the escalation of the Ukrainian crisis in February 2022, the Russian-European energy relationship underwent a dramatic shift. The market share of Russian natural gas in Europe plummeted from over 40% to around 10%. The volume of Russian gas delivered via Ukraine dropped from 40 billion cubic meters in 2019 to 15 billion cubic meters in 2023, as EU countries reduced imports and Ukraine closed one of its two Russian gas import routes.

Since the Crimean crisis, Russia has promoted the Nord Stream-2 pipeline as a complete alternative to Ukrainian gas transit to the EU. Despite being completed under U.S. sanctions and pressure, the Nord Stream-2 pipeline was ultimately put on hold when the German government suspended the inaugural review process.

Impact of ending the transit agreement on the parties

If the U.S. closes the gas pipeline to Russia, it would incur a loss of $800 million in transit revenues, roughly 0.5% of its GDP. Ukraine would then seek alternative gas sources, including reverse imports through the Trans-Balkan Pipeline, to meet its energy needs.

However, Russia stands to lose more significantly. With the U.S. transit channel cut off, the only remaining pipelines to Europe would be the Blue Stream and Turkish Stream, which supply gas from Turkey to the Balkan and Southern Europe regions. This scenario would result in Gazprom, already facing financial difficulties, having its gas exports halved, leading to an estimated loss of $7 billion to $8 billion in export revenue. More critically, Gazprom would struggle to fulfill long-term contracts with EU countries, which are valid until 2040. These contracts allow EU companies to pay for gas through Gazprombank, providing an umbrella of protection against U.S. and Western sanctions.

The European Commission’s REPower EU program aims to eliminate the use of Russian gas by 2027, but this prospect appears bleak. In May, Russian gas accounted for 15% of the EU’s total gas supply, surpassing U.S. gas imports for the first time since the escalation of the Ukraine crisis.

From 2026 onwards, significant volumes of liquefied gas from the U.S. and Qatar are expected to enter the European market. However, earlier this year, the Biden administration suspended authorization for new liquefying natural gas (LNG) projects to export to non-FTA countries, citing climate concerns. This decision could lead European buyers to question the long-term reliability of U.S. LNG supplies.

Among the EU countries most dependent on Ukraine for transit shipments of Russian gas are Austria, Slovakia, Hungary, and Italy. Austria and Italy are the least affected by disruptions in Russian gas supplies due to their diverse domestic pipelines. Italy can import gas from Algeria and Azerbaijan through pipelines and liquefied natural gas terminals, while Hungary can continue receiving Russian gas via the Turkish Stream pipeline. In contrast, Slovakia has limited options due to its location at the end of the supply routes.

Central and Eastern European countries are preparing for the potential termination of the Russian-Ukrainian gas transit agreement by promoting the creation of a ‘vertical gas corridor’ under the Central and South-Eastern European Gas Connectivity (CESEC). This corridor would leverage existing infrastructure in Ukraine and Moldova to enable liquefied gas imports from Greece and Turkey to reach Slovakia and Hungary. It also involves expanding the pipeline network in Southeast Europe, making Bulgaria a hub connecting Greece, Moldova, Turkey, and Ukraine. Europe’s unified energy market is expected to respond to ongoing geopolitical challenges through increased integration and expansion.

Eurasia’s gas trade landscape accelerates

Since the escalation of the crisis in Ukraine, the restructuring of the gas trade landscape in Eurasia has accelerated. Azerbaijan is striving to replace Russian gas supplies to meet EU demand.

As early as 2008, Azerbaijan’s Shah Deniz II gas field was identified as a source for the EU’s Southern Gas Corridor (SGC). The SGC, operational since 2020, is a crucial route transporting gas from the Caspian Sea to European markets, facilitating the delivery of Azerbaijani gas to Europe. Following the escalation of the Ukrainian crisis, the EU has actively collaborated with Azerbaijan, increasing gas deliveries annually. Some gas was partially piped through Ukraine, aiming to sustain Ukraine’s status as an energy transit country while reducing Russian gas imports.

In 2022, Azeri gas exports to Europe surged by 56%, making Azerbaijan one of the top three sources of piped gas imports to the EU in 2023. However, Azerbaijan faces challenges in fulfilling its ambitious export commitments, notably the need to boost production from its main gas field, Shah Deniz, and diversify gas sources, with Turkmenistan being essential for addressing its export challenges.

Turkey has long sought to position itself as an energy hub due to its geographical location, despite not being rich in hydrocarbons. As an EU candidate, establishing itself as a European gas hub would provide Turkey with geopolitical advantages, allowing it to align with European markets and extend its influence in the Black Sea and Mediterranean regions.

The ongoing crisis in Ukraine has expedited Turkey’s development as a gas hub, and following the Nord Stream explosion in October 2022, Turkey emerged as the largest importer of piped gas from Russia. Transitioning from a consumer nation at the edge of the European pipeline network, Turkey has become crucial for Russia to maintain its European market presence.

To secure alternative export routes to Europe, Russia has actively supported the establishment of a gas hub in Turkey and the creation of an electronic trading platform for determining gas prices. This hub-based trading process allows for the purchase of gas through the platform without revealing the exact source, enabling Russia to maintain a level of gas exports to Europe on an ‘anonymous’ basis.

Gazprom has already reached an agreement with Turkey on a roadmap for constructing a Turkish gas hub and has commenced implementation, including expanding traded gas volumes to accelerate the development of the Istanbul Energy Exchange. If Ukraine terminates its transit agreement with Russia by year-end, Russian pipeline gas will primarily reach Europe via Turkey. However, Russia’s capacity to significantly influence the establishment of a gas hub in Turkey is constrained by Europe’s resolve to decouple from Russian energy.

While the EU’s rising gas demand enhances Turkey’s prospects of becoming a gas hub, its success will depend on timely and effective implementation. Europe urgently needs alternative gas sources in the coming years, but overall demand for gas is likely to decline as the continent accelerates its energy transition. Considering this potential, Turkey’s future as a gas hub will likely evolve from a regional trading center in the European market to a global gas trading hub catering to various third parties, including the EU.

Source: ishizhi, Rystad Energy, Reuters, CEPA